Something fascinating is going on with HSBC, one of the world’s biggest banks, as the summer of 2019 continues to erupt around us. The timing of the developments is remarkable, in light of the connection of the other events to HSBC. Some of the connections are long-established and well known. Others are suggested by analysis of what appears to be going on right now.

The bottom line, however, is the appearance of a shadow “war” of some kind occurring – or, if not a war, at least an operation, with an apparent retreat and reorganization of forces underway.

The major collateral threads are the charges against Jeffrey Epstein, the ascent of Boris Johnson as leader of the Conservatives in the UK, and the increasing woes of China. Each of these threads bears tremendous portents for the future.

Whether China can stay the current course Xi Jinping has her on, and what the cost of that would be for China and the region – and indeed the world – hangs in the balance at this moment.

The Johnson government in the UK is the deciding factor for Brexit in October, the biggest geopolitical decision point Europe has faced since the collapse of the Soviet Union. It has already become clear that under Johnson, Brexit will not be a matter of unfavorable incrementalism for the Brits: a limp-along in a twilight zone of bad deals and quasi-independence from the EU. Johnson intends to make a real break – and as John Bolton clarified in his visit this week, the U.S. will be right there to support that policy.

As for the Epstein saga, its major portent is exposure, for a whole lot of people, and very likely for big companies and governments.

Epstein, financial bigwigs, and HSBC

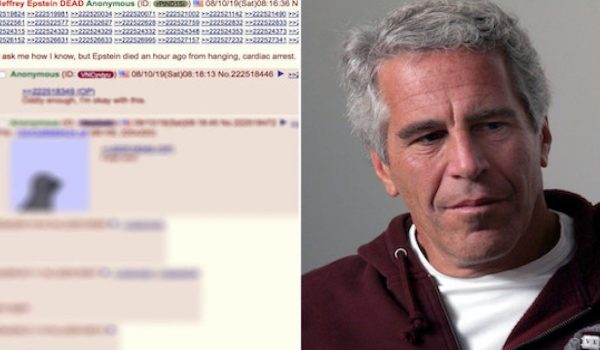

We see through a glass darkly right now, having a sense of what must be there, but not knowing what it will turn out to be when there’s black and white resolving itself under a floodlight. Epstein was closely connected to Bear Stearns, the investment firm whose demise presaged the mortgage-securities meltdown of 2008-09. He ran a fund called Liquid Funding Ltd, incorporated in the U.S. Virgin Islands, which suffered huge losses during the meltdown. At the same time that was happening, Epstein was being let off from serious sex-crime charges with a slap on the wrist, first by the state of Florida and then by the U.S. government.

Reportedly, he was cooperating in the investigation of Bear Stearns. Yet nothing ever really happened to executives at Bear Stearns, or indeed anyone else who might have been considered complicit in the seeming mismanagement of investments and capital holdings that produced the mortgage-securities collapse.

It’s hardly a conspiracy theory to look for answers on that to things like Epstein’s “little black book.” It’s merely obvious: what any competent law enforcement agency would do if faced with a similar situation. That black book has the names of a lot of people and entities that would have known, probably better than Epstein himself, what was going on – and wanted to keep others from knowing it.

Nor was the mortgage-securities collapse the only big financial event in which Epstein and the personalities in his black book figured, in the period before and after 2008-09. The fact that he did a lot of business through HSBC, that some of it was with the Clinton Global Initiative, that HSBC was the bank through which the “Panama Papers” leaks came out to the public in 2015, and Epstein and a list of interesting actors like the Clintons, Vladimir Putin, and others were revealed in them (as well as in the later leaks collected as the “Paradise Papers” in 2017) – all of these factors add freight to both the Epstein case and the fortunes of HSBC in 2019.

The Epstein case isn’t the only factor. But the potential for exposure from whatever happens with his case can’t be forgotten, as we try to parse the scramble in and around HSBC. That scramble burst out shortly after Epstein was taken into custody in July, and seems to have accelerated significantly in the weeks since.

An additional, historical point about HSBC, one that puts the Epstein factor in context, is the bank’s recurring role in money-laundering for global crime: not just terrorism and arms proliferation, but sanctions violation, particularly in the case of Iran’s nuclear program and arming of proxy forces abroad.

HSBC’s inability to stop doing this, in spite of being under U.S. government supervision in a deferred prosecution agreement from 2012 to 2018, has been – quite frankly – suspiciously chronic. It’s a big bank with a lot of moving parts, but nobody’s that slow on the uptake. The thought has had to intrude that “supervising” HSBC was less a burden for government authorities than an ongoing convenience; perhaps, for that matter, for more than one government.

There is extensively documented evidence, moreover, that HSBC has used the accounts of many, many small account-holders to facilitate the money-laundering, something the U.S. Congress was probing a few years ago and never got a satisfactory resolution on. These and other background facts are integral to interpreting what’s going on in 2019.

After Epstein

The most recent events are these. Epstein was arrested on 6 July 2019. That, by itself, would not have provoked the other events. But it has probably increased the urgency of the factors that did provoke them.

On 5 August, the CEO of HSBC, John Flint, was removed from his position by the board of directors after a short 18 months in the job. In the ensuing days, it has been reported that HSBC had been propping up the Chinese yuan and foreign currency reserves with major infusions of cash.

Dollar shortage is acute in China: this shouldn’t be a surprise at this point after #HSBC caught lending some $400-$700B to help China prop its dwindling #fx reserves AND Chinese state-owned #Banks (ie the #PBOC / #CCP) buying dollars in ONshore forward markets $USD #China

— Emma Muhleman CFA CPA (@EmmaCFA1) August 9, 2019

If the CEO of HSBC has been lending $400b USD to china to help them prop up their Monopoly money, that accounts for half of the reserves we have calculated that have already run. The chinese bank forward position on CNH is another $450 billion. Their currency is a HOUSE OF CARDS. https://t.co/sMjOJvdYY9

— 🇺🇸 Kyle Bass 🇹🇼 (@Jkylebass) August 7, 2019

In each case, notably, the story has been that Flint had to be removed because the Bank of England found out about the cash infusions to China’s central bank. That raises the question for me whether the BOE truly didn’t know, or – perhaps more likely – the change of government in Britain got around to affecting the BOE’s posture and priorities on this matter just before Flint was sent packing. If the latter, it’s probably because of (a) what’s happening in Hong Kong, and (b) recent consultations with the Trump administration.

In any case, HSBC is a very big bank, but banks are not “big” these days in relation to the great-power nations and their sovereign wealth funds. The latest market capitalization figure for HSBC Holdings is about $750 billion. The reported amount of cash infusions to China starts around $400 billion.

HSBC would be pointing a gun at its head and preparing to pull the trigger if it committed so much cash on its own initiative to propping up China’s currency position. We can confidently assume, if the reporting is valid, that someone put HSBC up to this. It would presumably be someone who expects complaisance from HSBC, and from whom HSBC has reason to expect a level of backstopping. That means it’s an entity the size of at least a G20 government, or perhaps more than one.

Shortly after Flint’s ouster was reported, the departure of other top officials – connected with operations in China – was announced. Helen Wong, CEO of the China branch and a 27-year veteran with HSBC, is out, and Mark McKeown, Chief Risk Officer for the Asia-Pacific region, was announced as retiring.

This three-fer is a major, attention-grabbing turnover. The interesting thing is that it is occurring at the same time as a massive restructure of the HSBC headquarters in the UK, which is attributed by analysts to the upcoming Brexit drama. Although HSBC is reportedly cutting some 4,000 jobs (not unusual in comparison with other rounds of job cuts in the last decade), the more significant move by far is shifting key elements of the HSBC regulatory compliance division from Britain to France.

The compliance arm hosts and works with the monitors who help HSBC comply with government orders like the Obama administration’s deferred prosecution agreement from 2012. (Jim Comey was briefly in such a supervisory role, at the U.S. branch of HSBC, back in 2013.)

For an international bank like HSBC, compliance is a huge aspect of doing business: an overhead cost for remaining eligible to operate under the authority of governments in the world’s most profitable economies. Moving compliance to the EU nation of France, just before Brexit, looks awful darn interesting.

It seems to suggest, at the very least, a concern by someone, somewhere, that the activities of the compliance division might not continue on exactly the same basis – whatever that basis has been – if Boris Johnson leads the Brexit and sets the priorities of the UK government after 31 October 2019.

The likelihood of closer cooperation with the U.S. at that point may factor into the equation. We get only whiffs of these events from outside the walls, but the most high-profile thing done by a U.S. supervisor (or monitor) of HSBC in recent months was tipping law enforcement off to Huawei executive Meng Wanzhou before she was detained by Canada in December 2018. That move infuriated Beijing, and seemed to have surprised a lot of other observers at the time.

There is reason to suppose, at least, if we cannot prove, that the Trump administration is monitoring HSBC with priorities different from those that may have prevailed in the past. (It may seem counterintuitive, but that is in part because the Trump administration has allowed some monitoring to sunset. One real possibility is that the current administration doesn’t have the same goals as the previous administration for keeping bureaucracy-linked supervisors in place at the bank.)

The scurry this summer to shift the compliance division at HSBC headquarters to an EU nation looks, frankly, like a salvage operation before the Brits execute a Brexit that will probably yield a closer alignment with U.S. policy on such matters – along with other matters of similar and related import.

https://twitter.com/HeshmatAlavi/status/1161327608404987904

That concern would be amplified for numerous interested parties by the prospect of uncontrollable exposures through the Epstein investigation. If I were in Epstein’s little black book, and knew about, or was a key player in, HSBC-related activities that folks would just as soon were sequestered tidily in France from now on, the last thing I’d want to see is Bill Barr coming over the hill at me. Years of funny money shenanigans are at stake here.

Hong Kong protests – and a slice of the U.S. investment posture there

Yet there is one more fascinating detail that seems related to the shadow machinations surrounding HSBC. It was alluded to briefly in an interview on Fox News on Tuesday night, during Shannon Bream’s show. The segment was about the protests in Hong Kong, and during a Q&A response, commentator Robert Spalding (Brig. Gen, USAF, Ret.) mentioned that the U.S. is funneling loads of cash through Hong Kong to the regime in Beijing, due to a move by index provider MSCI six months ago that significantly increased its emphasis on Chinese mainland shares in U.S. pension fund holdings.

(The whole interview is worthwhile, but start at 4:08 for the discussion outlined above.)

On its face, this move would seem to be shoring the Xi regime up, even as the Trump tariffs and the costs of unrest in Hong Kong take their toll.

But don’t forget the link suggested between John Flint’s ouster from HSBC, and HSBC reportedly doing something with a similar effect: funneling cash to Beijing to keep the currency propped up. Flint is gone because the Bank of England didn’t like that.

The two developments here literally cannot be unrelated. They are inherently related, whether we believe the decisions by the humans involved are knowingly connected or not. However the cash comes in, Beijing can use it to keep the yuan afloat – and keep at least a minimal reserve in U.S. dollars.

If the reporting is simply accurate on its face, what these two data points would mean is that the immediate stability of China’s financial situation has shifted its dependence: from whoever was behind HSBC’s currency-propping, to the good graces of the United States.

High stakes poker

If that shift has indeed occurred, we’ll know soon enough. Such a dependence raises the stakes exponentially for Xi’s decisions about how to proceed in Hong Kong. Cutting off a lifeline to a U.S. cash flow will have visible and extreme consequences for China, if the HSBC funnel-tunnel has been collapsed.

Trump might have a high card to play with China, but one that he would never outline to the public. If Xi finds a way to accommodate and pacify the protesters in Hong Kong, instead of mowing them down, it will be a good bet he was given a very powerful incentive to make that choice.

Perhaps this analysis misses the mark. We see but little from the outside. The facts, however, are mostly not in question; it’s the interpretation we can’t be certain of. Even if these factors and their interplay don’t explain what happens in China and Hong Kong in the next few days or weeks, they will be essential to some of our biggest geopolitical dramas in the months that follow. There’s a sense here of a shadow infrastructure beginning to collapse, one that encompasses a lot of territory and a lot of years.

We could say, with Churchill writing about World War II, that we aren’t seeing the beginning of the end, but the end of the beginning. I’m not convinced, however, that we’ve even reached the end of the beginning yet. I suspect that’s still to come.